Managing money can feel overwhelming, especially if you’re just starting your financial journey.

With so many budgeting methods available, many people struggle to find a system that is simple, flexible, and easy to follow over the long term.

This is where the 50/30/20 budget rule comes in.

Popularized by U.S. Senator and bankruptcy expert Elizabeth Warren, the 50/30/20 rule offers a straightforward way to divide your income between essential expenses, personal spending, and savings goals.

Rather than tracking every single purchase, this budgeting method focuses on allocating percentages of your after-tax income to three main categories.

In this guide, you’ll learn:

- What the 50/30/20 budget rule is

- How the rule works

- What expenses belong in each category

- The advantages and disadvantages of the method

- How to start using it in your own finances

- Common mistakes to avoid

Table of Contents

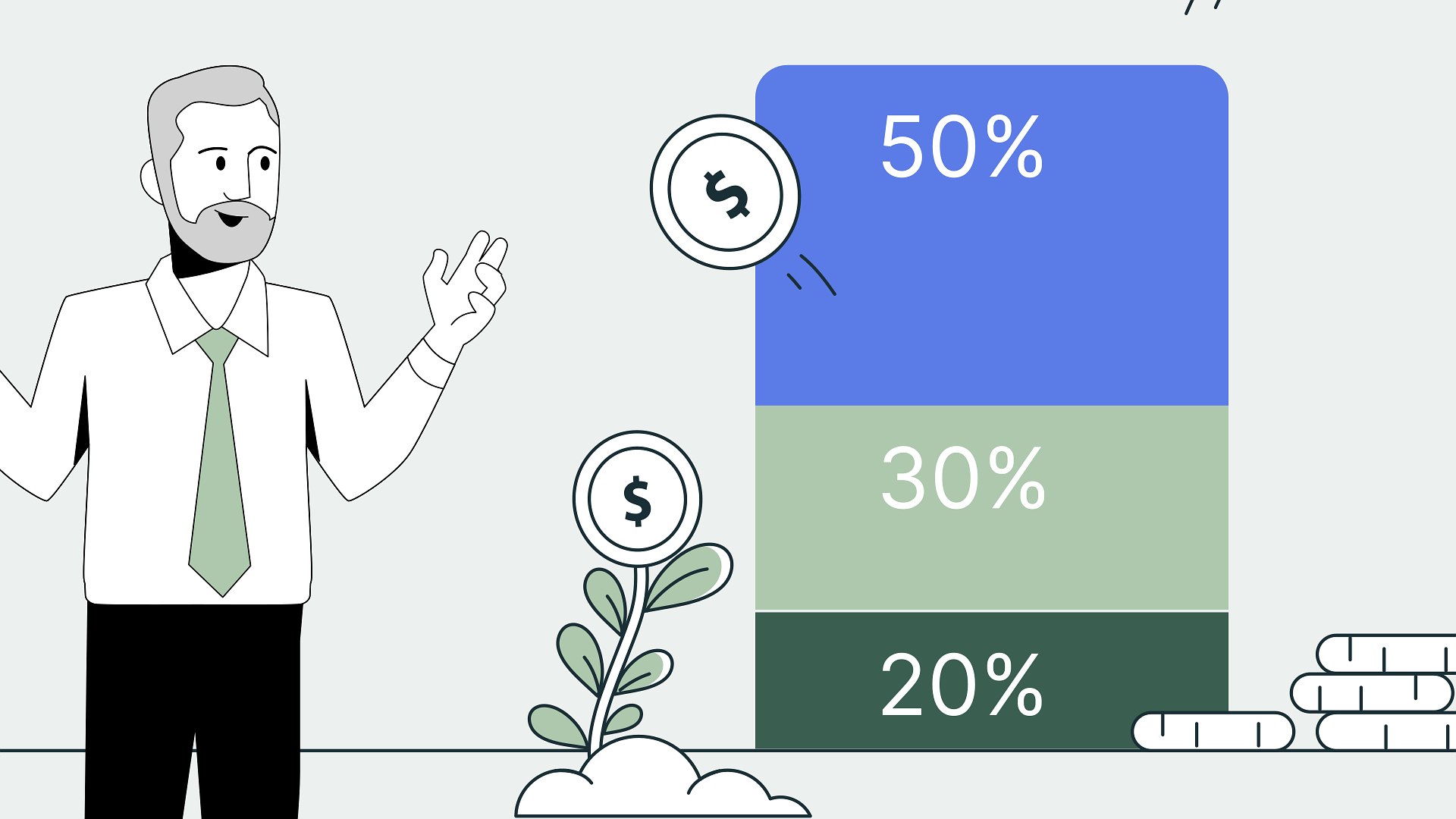

What Is the 50/30/20 Budget Rule?

The 50/30/20 budget rule is a budgeting strategy that divides your after-tax income into three categories:

- 50% for needs

- 30% for wants

- 20% for savings and investing

The goal is to create a balanced financial plan that allows you to cover essential expenses, enjoy your lifestyle, and continue building your financial future.

Unlike detailed budgeting systems that require tracking dozens of categories, the 50/30/20 method keeps things simple and sustainable.

This simplicity is one of the main reasons why the strategy has become one of the most popular budgeting methods in the world.

How Does the 50/30/20 Budget Rule Work?

The 50/30/20 budget rule divides your after-tax income into three simple categories.

This approach helps ensure that you cover your essential expenses, enjoy your money responsibly, and continue building your financial future at the same time.

Let’s break down each category.

50% Needs

The first 50% of your after-tax income should be allocated to essential expenses that you cannot avoid.

These are the costs required to maintain your basic standard of living.

Examples of needs include:

- Rent or mortgage payments

- Utilities

- Groceries

- Health insurance

- Transportation costs

- Minimum debt payments

- Childcare expenses

If your essential expenses exceed 50% of your income, you may need to consider reducing costs or increasing your income over time.

30% Wants

The next 30% of your income is reserved for non-essential spending that improves your quality of life.

These expenses are things you enjoy but could technically live without if necessary.

Examples of wants include:

- Dining out

- Streaming subscriptions

- Vacations

- Entertainment

- Hobbies

- Gym memberships

- Upgraded technology purchases

Many people confuse wants with needs, which is one of the main reasons budgets often fail.

Being honest about this category is essential for making the system work effectively.

20% Savings and Investing

The final 20% of your income should be directed toward improving your financial future.

This category includes:

- Emergency fund contributions

- Retirement savings

- Investment accounts

- Extra debt repayments

- Long-term financial goals

For many people, this is the most important category because it helps build wealth and financial security over time.

Even small contributions made consistently can grow significantly thanks to compound interest.

Example of the 50/30/20 Budget Rule

Let’s look at a practical example.

Imagine that your monthly after-tax income is $4,000.

Using the 50/30/20 budget rule, your money would be allocated as follows:

50% Needs = $2,000

This portion of your income would cover your essential expenses, such as:

- Rent or mortgage: $1,200

- Utilities: $200

- Groceries: $400

- Transportation: $150

- Insurance: $50

Total: $2,000

30% Wants = $1,200

This category covers discretionary spending and lifestyle choices:

- Dining out: $300

- Entertainment: $200

- Vacations: $300

- Subscriptions: $100

- Hobbies and leisure activities: $300

Total: $1,200

20% Savings and Investing = $800

This portion is dedicated to improving your financial future:

- Emergency fund contributions: $300

- Retirement savings: $300

- Investments: $200

Total: $800

| Monthly Income | Needs (50%) | Wants (30%) | Savings & Investing (20%) |

|---|---|---|---|

| $2,000 | $1,000 | $600 | $400 |

| $3,000 | $1,500 | $900 | $600 |

| $4,000 | $2,000 | $1,200 | $800 |

| $5,000 | $2,500 | $1,500 | $1,000 |

This example demonstrates how the 50/30/20 budget rule creates a balanced approach to money management by allowing you to meet your needs, enjoy your income, and build wealth at the same time.

Benefits of the 50/30/20 Budget Rule

The 50/30/20 budget rule has become one of the most popular budgeting methods in the world for several reasons.

Here are some of its biggest advantages:

Simple and Easy to Follow

One of the biggest strengths of the 50/30/20 rule is its simplicity.

Unlike traditional budgets that require tracking dozens of spending categories, this method only uses three broad categories.

This makes it easier to maintain over the long term.

Encourages Saving and Investing

Many people focus entirely on paying bills and spending money without setting aside anything for their future.

The 50/30/20 rule ensures that at least 20% of your income is dedicated to savings, investing, or reducing debt.

Over time, these contributions can significantly improve your financial security.

Provides Financial Flexibility

The budget allows room for enjoyment and lifestyle spending without creating guilt or stress.

By allocating 30% of your income to wants, you can enjoy your money while still making progress toward your financial goals.

Helps Prevent Overspending

Many people spend money without realizing where it goes each month.

The 50/30/20 rule creates clear limits for each spending category, making it easier to identify unhealthy spending habits.

Works for Most Income Levels

Whether you earn $2,000 per month or $20,000 per month, the percentages remain the same.

This makes the system highly adaptable and easy to scale as your income grows.

Potential Drawbacks

Although the 50/30/20 budget rule works very well for many people, it is not perfect for every financial situation.

Understanding its limitations can help you decide whether this budgeting method is right for you.

It May Not Work in High-Cost Areas

In cities with a high cost of living, essential expenses such as rent and transportation can easily exceed 50% of your income.

This can make it difficult to follow the rule exactly without making significant lifestyle adjustments.

Low-Income Households May Struggle

For individuals or families with lower incomes, covering basic necessities often takes priority over saving or discretionary spending.

In these situations, the percentages may need to be adjusted to reflect financial reality.

It Doesn’t Track Spending Categories in Detail

Some people prefer a more detailed budgeting system that tracks spending in multiple categories.

The 50/30/20 rule focuses on broad spending groups rather than individual expenses, which may not provide enough detail for everyone.

Financial Goals May Require Different Allocations

If you are aggressively paying off debt, saving for a house deposit, or preparing for retirement, you may decide to allocate more than 20% of your income toward savings and investments.

The 50/30/20 rule should be viewed as a guideline rather than a strict rule.

Every Financial Situation Is Different

Personal finance is personal.

The ideal budget depends on your income, location, family responsibilities, and financial goals.

The most important factor is creating a system that you can realistically maintain over the long term.

How to Start Using the 50/30/20 Budget Rule

Getting started with the 50/30/20 budget rule is surprisingly simple.

Follow these steps to apply the method to your own finances:

Calculate Your After-Tax Income

The first step is determining how much money you actually receive after taxes and deductions.

If your monthly take-home pay is $3,500, that is the number you will use for your budget calculations.

Track Your Current Spending

Before making any changes, review your spending habits over the last one or two months.

This will help you understand how much you currently spend on needs, wants, and savings.

Many people are surprised to discover where their money is actually going.

Divide Your Spending Into Categories

Separate your expenses into the three categories:

- Needs

- Wants

- Savings and Investing

This will allow you to compare your current spending habits with the recommended percentages.

Make Adjustments Gradually

If your current budget does not match the 50/30/20 allocation, don’t panic.

Very few people fit perfectly into these percentages immediately.

Instead, make gradual improvements over time by reducing unnecessary spending or increasing your income.

Review Your Budget Regularly

Your financial situation will change over time.

Salary increases, moving home, marriage, or having children can all affect your budget.

Reviewing your finances every few months helps ensure your budget continues to match your goals and circumstances.

Common Budgeting Mistakes

Creating a budget is an important step toward financial stability, but many people make mistakes that prevent their budget from working effectively.

Here are some of the most common budgeting mistakes to avoid:

Underestimating Expenses

One of the biggest budgeting mistakes is assuming that monthly expenses are lower than they actually are.

Small purchases, subscriptions, and occasional expenses can quickly add up and throw your budget off track.

Tracking your spending accurately is essential.

Confusing Needs and Wants

Many people classify wants as needs.

For example, while transportation may be a need, owning a luxury car is usually a want.

Being honest about the difference between needs and wants is one of the keys to making the 50/30/20 budget rule successful.

Not Including Savings as a Priority

Many people save whatever money is left over at the end of the month.

Unfortunately, there is often nothing left to save.

Instead, savings should be treated like any other monthly expense and included in your budget from the beginning.

Ignoring Irregular Expenses

Expenses such as holidays, insurance renewals, car maintenance, and home repairs do not occur every month, but they should still be included in your financial planning.

Setting aside money for these expenses can prevent unpleasant surprises later.

Giving Up Too Quickly

Budgets rarely work perfectly during the first month.

Adjustments are normal and expected.

The goal is not perfection but consistency and gradual improvement over time.

The most successful budgets are the ones that people can realistically maintain for years, not just a few weeks.

Frequently Asked Questions

Is the 50/30/20 budget rule good for beginners?

Yes. The 50/30/20 budget rule is considered one of the best budgeting methods for beginners because it is simple, flexible, and easy to understand.

Unlike more detailed budgeting systems, it only requires tracking three categories of spending.

What if my needs are more than 50% of my income?

This is very common, especially in areas with a high cost of living.

If your essential expenses exceed 50% of your income, try to gradually reduce costs or increase your income over time. The percentages should be viewed as guidelines rather than strict rules.

Does the 20% include investing?

Yes.

The 20% category includes:

- Emergency fund contributions

- Retirement savings

- Investments

- Extra debt repayments

- Other long-term financial goals

Can I adjust the percentages?

Absolutely.

Personal finance is personal, and your budget should reflect your own circumstances and goals.

Some people may prefer a 60/20/20 budget, while others may use a 50/20/30 approach depending on their situation.

Is the 50/30/20 budget rule better than zero-based budgeting?

Neither budgeting method is universally better.

The 50/30/20 rule focuses on simplicity and flexibility, while zero-based budgeting provides greater control and detail.

The best budgeting system is the one that you can consistently follow over the long term.

Conclusion

The 50/30/20 budget rule is one of the simplest and most effective ways to manage your money.

By dividing your income into needs, wants, and savings, you can create a balanced financial plan that supports both your current lifestyle and your future goals.

While the exact percentages may not work perfectly for everyone, the framework provides an excellent starting point for building healthier financial habits.

The key to successful budgeting is not perfection but consistency.

Small improvements made over time can lead to significant financial progress in the future.

Whether your goal is to build an emergency fund, start investing, buy a home, or achieve financial independence, having a clear budget is one of the most powerful tools you can use.

The best budget is not necessarily the most detailed one. It is the one that you can realistically follow month after month.

Start today, make adjustments as needed, and focus on long-term progress rather than short-term perfection.